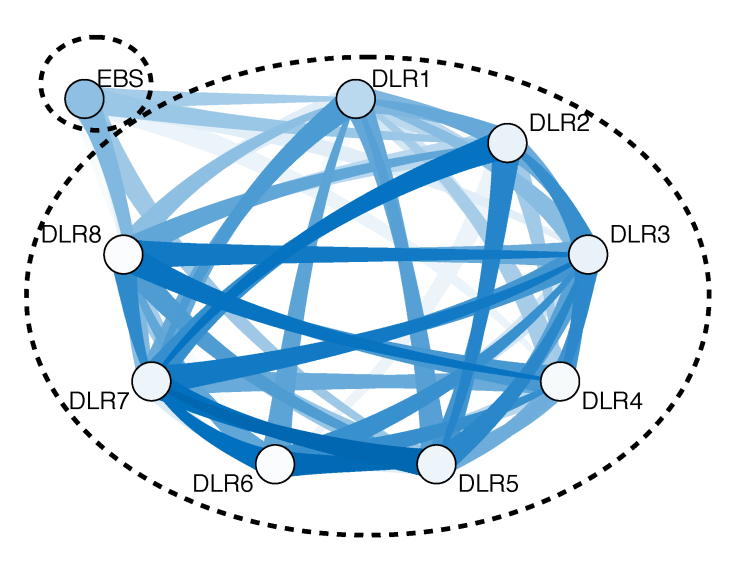

When the trading of a security is fragmented across exchanges, MTFs, and dark pools, the prices at different markets co-move almost instantaneously. Almost. What happens in the time span specified as almost instantaneous? Once new information appears at one market, how does it spread to the other markets trading the same security?

Information percolation describes how information spreads between markets. In a paper with Albert Menkveld, we propose a new methodology to measure information percolation in ultra high-frequency data, uncovering the paths information flows take between markets. We apply it to the euro-Swiss franc currency pair, showing how information flows between dealers at the OTC market and the interdealer trading platform EBS.

The paper is at SSRN, and a longer blog post is at Albert’s website.