At the opening of US equity markets on August 24, 2015, prices dropped sharply following overnight turmoil in global markets. In the minutes after opening, large order imbalances triggered circuit breakers to halt trading in numerous stocks and exchange-traded funds. More than a thousand securities were affected and hundreds of them experienced repeated trading halts before prices stabilized.

Large price moves at the market opening is nothing new. To effectively incorporate overnight news in prices, equity markets typically open with a batch auction that aggregates trading interests and establishes an equilibrium price. What caused chaos on August 24, 2015, is that many opening auctions apply price collars, disallowing extraordinary price moves in the auction mechanism. The consequence is that large imbalances spillover to the continuous trading, where continued price swings trigger circuit breakers. In response to this problem, US exchanges—including NASDAQ, NYSE, and NYSE Arca—have suggested replacing auction price collars with another type of volatility curb: a volatility extension.

In a new paper that I coauthor with Ester Félez Viñas, we analyze the merit of Call Auction Volatility Extensions (CAVEs). The mechanism works as follows. If there is a large price change during the batch auction, the order entry phase (the batching period) is extended to allow investors to reconsider their orders. Instead of constraining price discovery (like price collars do), the volatility extension delays it.

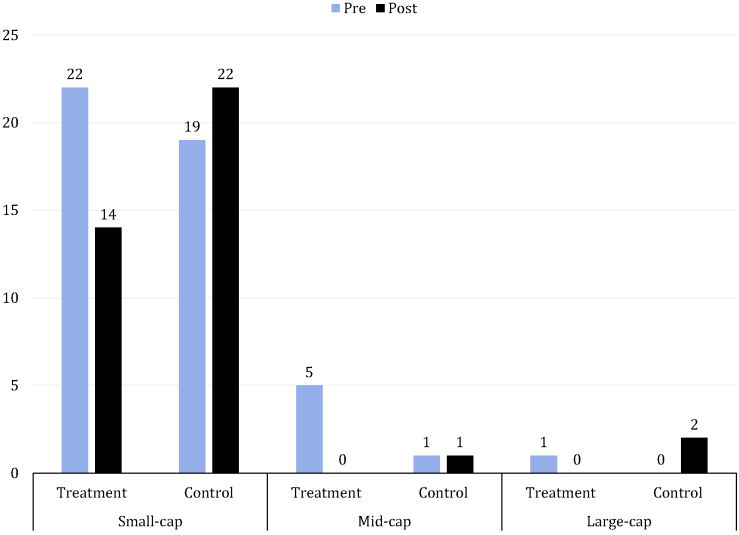

We study the introduction of CAVEs in the closing auction at NASDAQ Stockholm. On December 1, 2014, NASDAQ introduced CAVEs for its Stockholm segment, while the Copenhagen and Helsinki segments were unaffected. The introduction thus provides us with a nice benchmark.

The figure below shows the incidence of extraordinary volatility events before and after the introduction of CAVEs. It is evident that the extraordinary volatility incidence drops substantially in the Treatment market (NASDAQ Stockholm), in particular for small-caps. The finding is corroborated by that the Control markets (NASDAQ Copenhagen and Helsinki), where no CAVEs are introduced, do not show the same effect.

In the paper we also analyze why extraordinary volatility is reduced. We hypothesize that CAVEs reduce the risk of market abuse and that it increases investors’ trust in the auction mechanism, and present supportive empirical evidence.

The paper is available at SSRN.